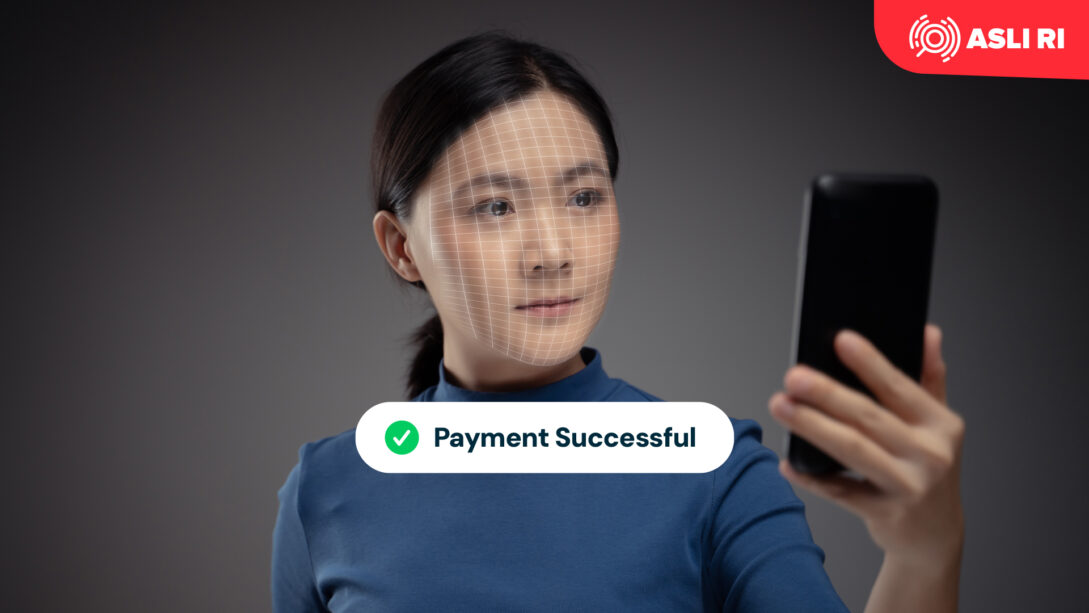

The way we pay has evolved dramatically in the past decade. From cash to cards, from mobile wallets to QR codes — and now, to biometrics. Consumers are increasingly comfortable using their fingerprint or facial recognition to approve transactions on their smartphones.

Yet behind the convenience lies a question that leaders in banking and fintech cannot ignore: is relying solely on device-based biometrics enough to secure high-value and high-volume transactions?

This is where ASLI AuthentID comes in, providing server-side biometric verification that goes beyond the limits of consumer devices.

Device Biometric vs. Server-Side Biometric Verification

When a customer uses Face ID or fingerprint on their phone, the biometric data never leaves the device. This ensures privacy but comes with trade-offs:

- Transaction limits: Device-only verification is often capped at low-to-medium transaction values.

- Limited cross-channel use: Biometrics stored on a phone cannot be used seamlessly for ATMs, desktops, or branchless banking.

- Inconsistent standards: Different devices have different levels of security, making it hard for financial institutions to maintain compliance.

Server-side biometric verification addresses these gaps by enabling real-time authentication through an external verification engine such as ASLI AuthentID.

Why Server-Side Biometrics Matters

With server-side verification, the process works as follows:

- The user captures a selfie or fingerprint scan.

- The system converts the image into an encrypted, temporary biometric template — processed only for that transaction.

- The template is transmitted securely to ASLI AuthentID for liveness detection, anti-spoofing checks, and database matching.

- The verification result (yes/no) is returned instantly to the bank or fintech, while the biometric data is immediately discarded.

Unlike common concerns around “data extraction,” ASLI AuthentID never stores biometric data. It functions as a real-time verifier, not a data repository. This ensures compliance, security, and most importantly, trust.

Advantages for Financial Institutions

For banks, e-wallets, and payment providers, the shift to server-side biometric verification brings tangible advantages:

- Enhanced Security: Protection against spoofing, deepfakes, and stolen credentials.

- Higher Transaction Thresholds: Confidently approve higher-value transactions without relying on PINs or OTPs.

- Omni-channel Consistency: One biometric identity works across mobile, ATM, desktop, and even in-branch.

- Regulatory Compliance: Meet stringent KYC, AML, and data protection standards with a privacy-first approach.

Case Study: ASLI Loyal at the Workplace Café

At ASLI RI, we have already tested this technology in a real-world environment. Internally, our team launched ASLI Loyal, a loyalty and biometric payment solution integrated with ASLI AuthentID.

Here’s how it works:

- Employees order their coffee directly through WhatsApp — choosing to pick it up or have it delivered to their floor.

- During checkout, the system requests biometric verification using ASLI AuthentID.

- Once confirmed, the payment is processed instantly, without the need for cash or cards.

This simple integration transformed our office café into a showcase of frictionless, secure, and delightful payment experiences. It proved that biometric payments are not just a vision for the future but already practical today — scalable, privacy-compliant, and ready for adoption by enterprises.

Conclusion: A Smarter Future for Payments

Biometric authentication is no longer just about unlocking smartphones. With solutions like ASLI AuthentID, organizations can embed biometrics into their payment flows in a way that is secure, compliant, and user-friendly.

For financial leaders, the question is not if biometric payments will go mainstream, but when and how they will adapt. ASLI RI’s commitment to real-time verification, zero data storage, and enterprise integration ensures that this transition can happen smoothly — delivering both convenience for users and confidence for institutions.

Last modified: September 11, 2025