Indonesia’s neobanking sector is experiencing a surge in popularity, although its exact market share remains uncertain. Jenius, a prominent neobank, boasts over 8 million users as of February 2024, showcasing impressive growth since its launch in August 2026. While an exact timeline and initial user base are unclear, this significant user increase highlights the potential of neobanks within the Indonesian market.

Challenges and Security Concerns

The path to technological advancement is not without hurdles. Fintech companies operating neobanks must remain vigilant against digital fraud and cybercriminals who constantly threaten user safety. This article explore how fraud manifests in neobanking and proposes potential strategies to eliminate these risks.

Neobanking, A New Iteration of Banking

The emergence of neobanks can be traced back to the aftermath of the 2007-2008 global financial crisis, a period that significantly eroded consumer trust in conventional banks. What truly sets neobanks apart is their complete absence of physical branches. All operations are conducted entirely online. This digital approach also eliminates the need for ATMs, making neobanking accounts significantly cheaper to establish due to the absence of ATMs fees and branch maintenance costs. Here are some additional reason why people might prefer neobanking:

- Unmatched convenience. Neobanking can be accessed via mobile phone apps, requiring only a decent internet connection, such as cashback and merchant promotions, to entice users towards their services.

- Competitive interest and benefits. Neobanks often offer competitive interest rates and numerous benefits, such as cashback and merchant promos that could entice users to use their services.

- Tailored solutions. Neobanking offers support for a wide range of customer segments, unlike conventional banks, they can cater to the specific needs of small businesses, freelancers, and other niche markets.

Market Insights and Potential Risks

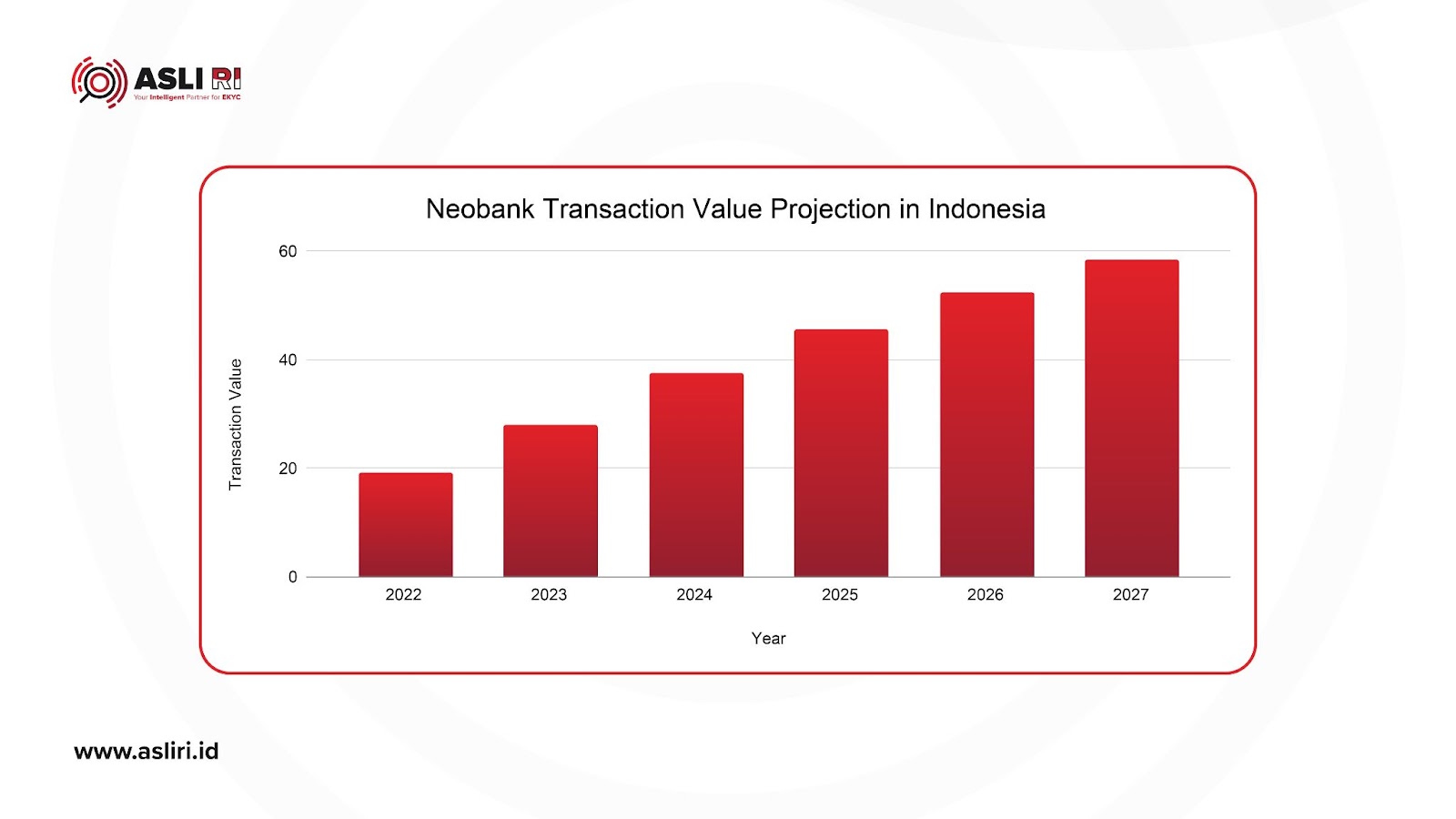

According to a market insight analysis by Statista April 2023), the transaction value of neobanks in Indonesia is projected to climb to a staggering US$58.38 billion by 2027. However, the same analysis reveals that user penetration for neobanking was only 3% nationwide as of 2023, with projections indicating a rise to 4.4% by 2027. This relatively low user penetration rate suggests that each existing neobank user contributes to a larger transaction value.

With vast sums of money flowing through Indonesian neobanks, cybercriminals are constantly on the lookout for opportunities to exploit these systems.

How Can Fraud Occur in Neobanking?

Neobanking’s complete reliance on digital processes creates vulnerabilities that cybercriminals can exploit to commit various types of digital fraud. Here are some common forms of fraud that can plague neobanking:

- Phishing or social engineering. This tactic deceives victims into revealing personal information through illegitimate means. Fraudsters may send fraudulent emails or create fake websites impersonating legitimate neobank providers to steal passwords of PINs.

- New account fraud. This involves using a stolen, fraudulent, or synthetic identity to create a new neobank account.

- Account takeover fraud. This occurs when fraudsters gain unauthorized access to a legitimate neobank account. They might achieve this by using phishing tactics or malware to steal passwords.

These fraudulent activities may seem like minor inconvenience, but underestimating the capabilities of cybercriminals is a grave mistake. Fraudsters can exploit illegitimate neobank accounts to launder money for illegal purposes, ranging from smuggling illicit substances to human trafficking.

The vast majority of neobanking fraud can be categorized as identity theft, which involves stealing or creating a fake identity to impersonate someone else. Fortunately, there are measures you can take to prevent identity theft.

Neobanking Fraud Prevention Measures

Implementing measures against fraud in neobanking is especially important to ensure the safety of user’s data and funds. That can be done by:

- Implementing identity verification measures. Before opening an account, prospective users must complete an identity verification process to ensure that their data matches the information given. This can be done through EKYC and liveness detection procedures.

- Employing a robust authentication and verification system. These days, a simple password is not enough to rat out fraudsters. Multi-factor authentication (MFA) using biometric verification or SMS-based OTPs can help ensure an even stronger layer of security.

- Implementing fraud detection. Utilizing artificial intelligence, suspicious behavior associated with fraud can be detected, enabling further use of the Neo-bank account to be blocked.

- Complying with local policies. Different countries have different data security policies, which can range from requirements to implement security systems or requirements to conduct routine audits.

Explore the Future of Banking with Confidence!

Neobanking propels Indonesia into a future where digital transformation is the norm. As more and more people become digitally literate, the usage of digital banks, marketplaces, and other conveniences could increase exponentially. With projections predicting that the market for neobanks will increase in the next half decade, neobank operators must be constantly aware of the threat of fraud.

ASLI RI is the perfect partner for you to squash fraudsters. Our True Identity Assurance technology is curated to include the necessary tools you need in your fight against fraudsters. Digital security is our utmost priority. For more information, contact our team through www.asliri.id/contact!

digital banking Neobank Security

Last modified: May 15, 2024