Have you ever considered integrating Buy Now Pay Later (BNPL), locally known as pay-later, into your business platform? This short-term financing option is gaining popularity among businesses. BNPL empowers your customers to make purchases and defer payments in fixed installments, commonly associated with online marketplaces. It’s not limited to consumer products; BNPL can be applied to various transactions, from travel bookings to bill payments. As a business owner, integrating BNPL can enhance the shopping experience for your customers. However, it’s crucial to be aware of potential fraud risks associated with this payment method. Read this article to understand how pay-later fraud works and what measures you can take to safeguard your business.

But First, How Popular are Pay-Later Services?

Pay-Later fraud works almost like a mix of credit card and e-commerce fraud. Here are some common tactics associated with pay-later fraud:

- Fake account fraud. Fraudsters use stolen or fraudulent identities to create a fraudulent account, in which they can purchase as many items as possible before authorities flag them as threats.

- Account takeover (ATO) fraud. Fraudsters take over a genuine account and use it to purchase items, they leave it to the actual account owner to pay the bills.

- Chargeback abuse fraud. Fraudsters ask for a refund over a purchase that they don’t recognize.

With the methods above, the fraudsters would be harder to track since their identity isn’t associated with the pay-later account. There are also fraud tactics that are unique to pay-later services. These are:

- Fraudulent pay-later platforms. Fraudsters create a website that looks like a legitimate pay-later service provider. The website then tricks unsuspecting users into registering for its service, giving the fraudsters their personal information like their ID cards and addresses.

- Pay-later phishing. This fraud tactic involves fraudsters posing as legitimate customer service agents of a pay-later platform messaging users about limit disbursement or other services. The fraudulent agent would then ask the victim for their credentials, which the fraudster can use to access the victim’s pay-later account.

The graph above from a survey done by Callsign shows the types of fraud that pay-later users have experienced. Of the people surveyed, 1 in 4 people have experienced pay-later fraud, identity theft (opening pay-later accounts using the victim’s stolen identity) being the most common

So, What Can You Do to Prevent Pay-Later Fraud?

Raising awareness of common fraud tactics is one preventive approach to handling pay-later fraud. As more people are aware of the fraud tactics, they will be less likely to fall prey to it in the future.As most pay-later fraud instances involve stealing and misusing personal identity, investing in a more secure identity verification system is the most suitable thing for any business to do to protect customer data and prevent identity misuse. An example of a technology that can be used to protect customer data is digital onboarding. This system can be used to seamlessly onboard users while simultaneously verifying identity and documents.

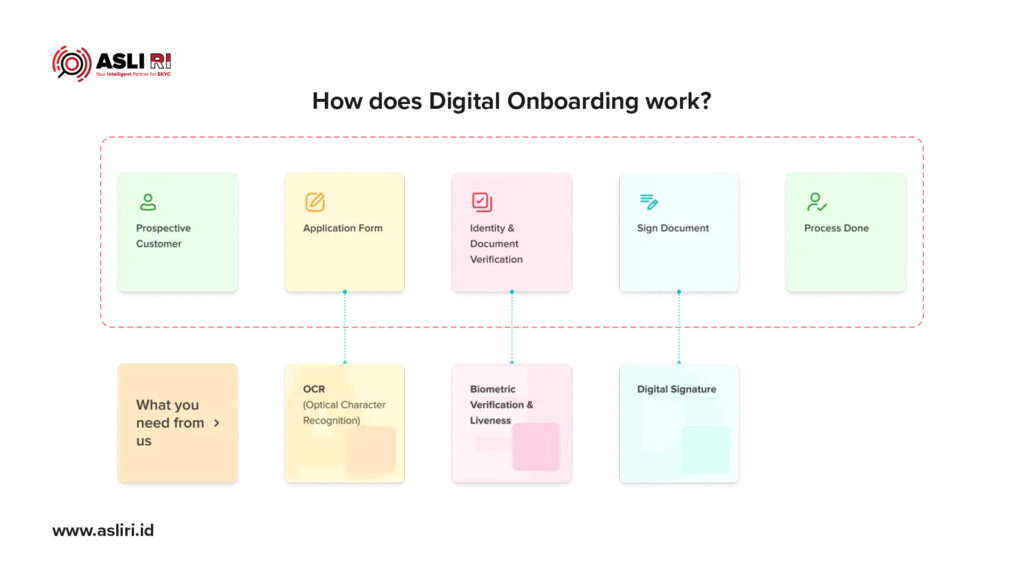

The image above shows how ASLI RI’s digital onboarding system works. It is hassle-free and easy to use anywhere and at any time. Firstly, the prospective user fills in an application form to register for the pay-later service. This process is where the user submits a photograph of their identity card, themselves with their identity card and any other required documents. The system then uses optical character recognition (OCR) to match the data on the form and the documents. After that, the system conducts identity and document verification, biometric verification, and liveness detection to ensure that the person who submitted the photo and documents is who they say they are. This process eliminates spoof attacks and identity manipulation. After the prospective customer clears all checks, the prospective customer can sign the required documents using a digital signature. Digital onboarding is more secure and is suitable for pay-later platforms that operate digitally.

As a user, there are also steps that you can take to prevent being a victim of pay-later fraud. These include making sure that you use a pay-later platform that is regulated and registered to Otoritas Jasa Keuangan (OJK), not clicking on any suspicious links or engaging with suspicious customer service agents, and not handing out your credentials to anyone.

Create a safer business ecosystem with ASLI RI

The popularity of pay-later usage is at an all-time high and will only increase over time. With this comes the responsibility to protect customer data from misuse by fraudsters. To protect customer data from misuse, pay-later providers need to take steps to secure their systems and educate their customers about the risks of fraud. ASLI RI can be your partner in establishing a safe and secure digital ecosystem.

Want to learn more about our products and how you can use them in the fight against fraudsters, visit www.asliri.id/contact to request a product demo that suits your business’ needs.

Business Security buy now pay later fraud Digital Onboarding pay-later fraud prevention

Last modified: November 27, 2023